Modern, and especially mobile, technology has offered challenges to the traditional brick-and-mortar branches of banks and credit unions. However, the in-person banking experience continues to be surprisingly relevant, even in the era of digital convenience. Below, we will outline why, as well as the ways your own branch transformation will keep your clients returning and satisfied.

Who goes to bank branches, and where?

Typically planted in towns near shopping, restaurants, gas stations, and other higher-traffic areas, branches are located for community convenience. In 2018, the Federal Reserve completed a study entitled “The Branch Puzzle: Why Are there Still Bank Branches?”, which analyzed the clients of physical bank and credit union branches. The findings indicated that while most clients touch online banking in some way, the most “frequent fliers” of physical branches included the older population, the wealthier percentile, and those who are self-employed. While each category’s needs vary in nature and complexity, their attachment to physical branches persists.

Three reasons branches continue to be relevant

- Opening new accounts and loan products: Future Branches says, “’Research reveals most customers prefer branches over digital channels when opening new accounts for both simple (such as savings accounts and debit cards) and complex products (such as loans),’ reports Deloitte Insights.” Branches can support life events, such as purchasing or renovating a home, opening an account for clients or their family members, or starting a business. In many cases, the loans and terms available are incredibly complex, so having literature and explanation can smooth out the process.

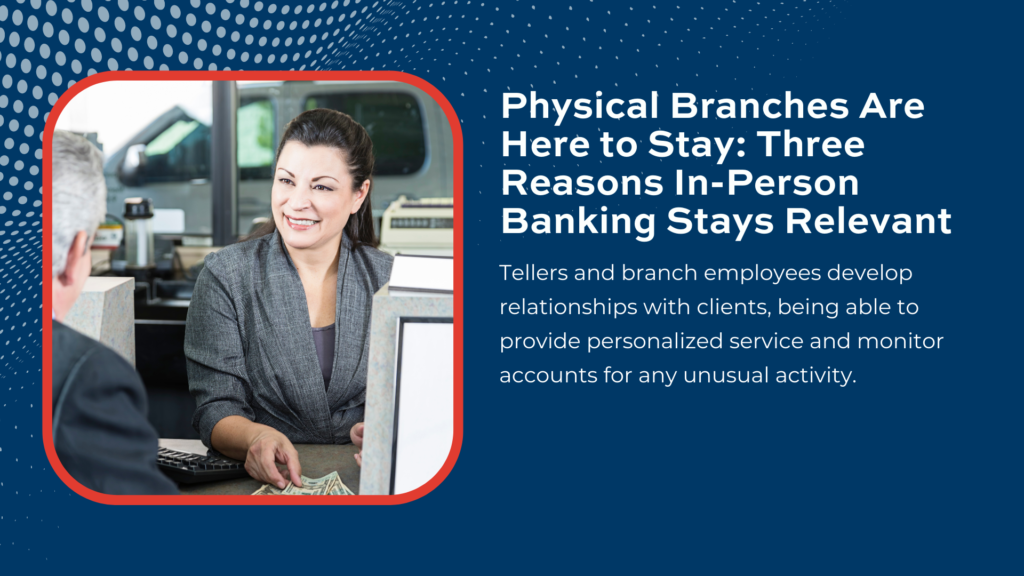

- Trust and human experience: In an editorial, Fintech executive David Horton says, “It’s a place where customers can speak face to face with someone about something that is pretty important – money. It’s difficult to not reiterate how important that is, because it’s only when things go horribly wrong that you can truly appreciate this point.” Tellers and branch employees develop relationships with clients, being able to provide personalized service and monitor accounts for any unusual activity. Also, branch employees can provide financial advice and guidance, which can be inconvenient or even impossible to achieve within the confines of a mobile app.

- Access to cash: In areas and demographics in which the use of cash is particularly prevalent, cash withdrawal services both inside the branch and outside at an ATM or ITM accomplish what a mobile app cannot. Marketplace.org explains, “…despite the rise of online banking, physical banks still retain a presence in some communities. There are still many people (especially those who skew older) who aren’t used to managing their finances electronically, while some of the services that banks provide still require face-to-face interaction, according to Jaime Peters, assistant dean and assistant professor of finance at Maryville University of St. Louis. ‘Additionally, we’re still a fairly large cash society, and you have to have a branch, especially if you’re a small business, and you’re dealing with cash in and cash out,’ Peters said.”

What can branches do to remain competitive?

- Adopt new ATM or ITM technology: Wittenbach partner Hyosung’s products, such as the cutting-edge 8300 series ITMs or more cost-conscious Series 7 ATMs, feature a sleek user experience on current Windows 10 technology, and are a great addition during a branch transformation. The ITMs also include cash recycling and video teller functionality which provide efficiency and ensure that your client is supported as they withdraw cash, make deposits, and consider other loan or credit products.

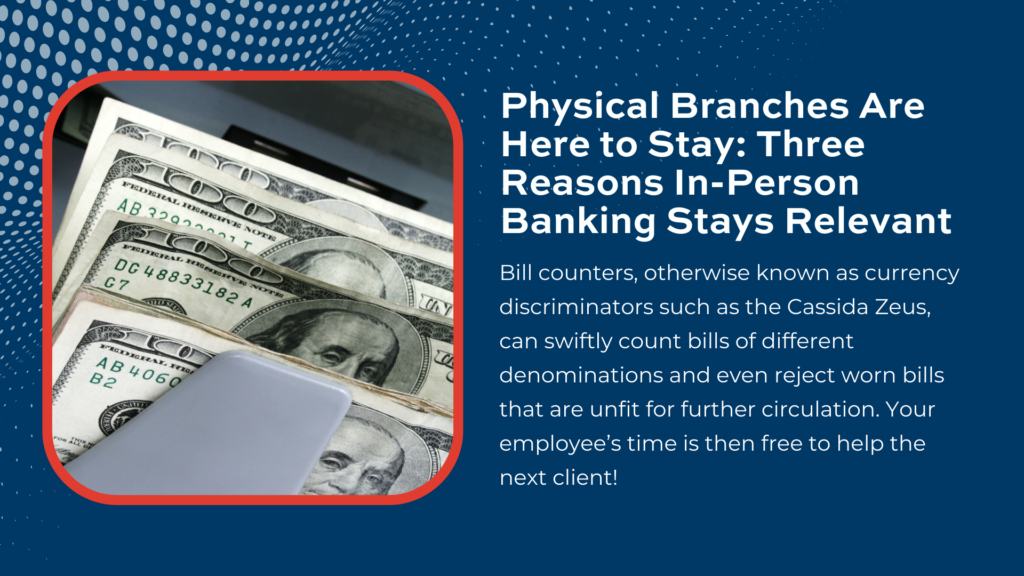

- Drive efficiency with bill counters: When your branch employees no longer have to manually count cash, their job can be done with precision and timeliness. Bill counters, otherwise known as currency discriminators such as the Cassida Zeus, can swiftly count bills of different denominations and even reject worn bills that are unfit for further circulation. Your employee’s time is then free to help the next client!

- Keep a pulse on security: By installing a Network Video Recorder (NVR) system, your branch can improve on the lower-resolution Digital Video Recorder (DVR) systems as they run on wireless internet and can store data on the cloud. Systems such as the Verint EdgeVR use IP cameras with face recognition technology to deter crime and keep your branches safe.

- Health and safety focus: The Banking Journal recommends products such as infrared mirrors if you have a policy of temperature checks to potentially detect illness, and density sensors to manage the flow of traffic. In the current state of the Covid-era world, this may not be immediately necessary; however, the technology is now readily available. If needed in the future during a branch transformation, these measures can help keep your customers comfortable to enter your branch.

Conclusion

When your branches can anticipate the needs and questions of those in your communities, the need for in-person customer service will remain evergreen. While the technological landscape is transforming the way financial institutions interact with clients, your branch can remain competitive by optimizing the time and value of each interaction, while keeping your employees and customers safe. Contact Wittenbach for more best practice advice on branch transformation and outfitting your branch for the future!