As the breadth and depth of fintech services grow, there is a continued need to connect with other services, including banks and credit unions. Doing so enables banking as a service (BaaS) offerings such as branded reward cards or adding payment functionality to their apps.

BaaS offerings have driven the fintech space to a total valuation of $179 billion, nearly double where it was in 2017.

None of this rapid growth would be possible without banking APIs, which bridge the gap between banks and fintech, allowing the two financial services to “talk” to each other, transmitting consumer data from one platform or application to another.

Additionally, APIs not only increase functionality between platforms, they can also improve your bank’s security. But what exactly is API?

What Is API?

API is an acronym for application programming interface. An API allows two applications to talk to each other, with the API acting as an intermediary. APIs are commonly used in many applications, such as rideshare apps, weather apps, and banking apps. When you use one of these apps, it connects to the internet, sending data to a server. The server then retrieves that data, performs the needed actions, then sends it back to your phone or other device. The application then interprets that data and provides you with the requested info.

APIs allow for data to be communicated securely. In the given example, both your mobile device and the server are never fully exposed to each other. The data transmitted is only via small packets of data that share only what is absolutely necessary.

Why Do Banks Use APIs?

APIs are versatile, and prevalent in the tech world. Banking APIs allow banks and other financial institutions to communicate with each other, securely.

A common example of banking API use is aggregating accounts from different financial institutions. This allows a customer to see all of their accounts, such as checking, savings, retirement funds, and other investment accounts and holdings, all in one place. Getting access to all of these accounts in one place versus having to log into each account individually offers a valuable customer convenience. In essence, from one login, a customer gets to see an entire portfolio, saving time and offering greater security.

Banking APIs are also used for other services such as subscription management, helping a customer find the closest ATM, or providing other personalized financial services, such as their spending or saving habits, or gaining access to statements.

Banking APIs are used for open banking, too. Open banking is a service that shares a customer’s data, as per a customer’s preference and permission, between a bank and a third-party financial institution. This data could include the customer’s name, account information, and other sensitive data. APIs create the security needed for the transmission of this kind of data sharing.

How APIs Can Improve Banking Security

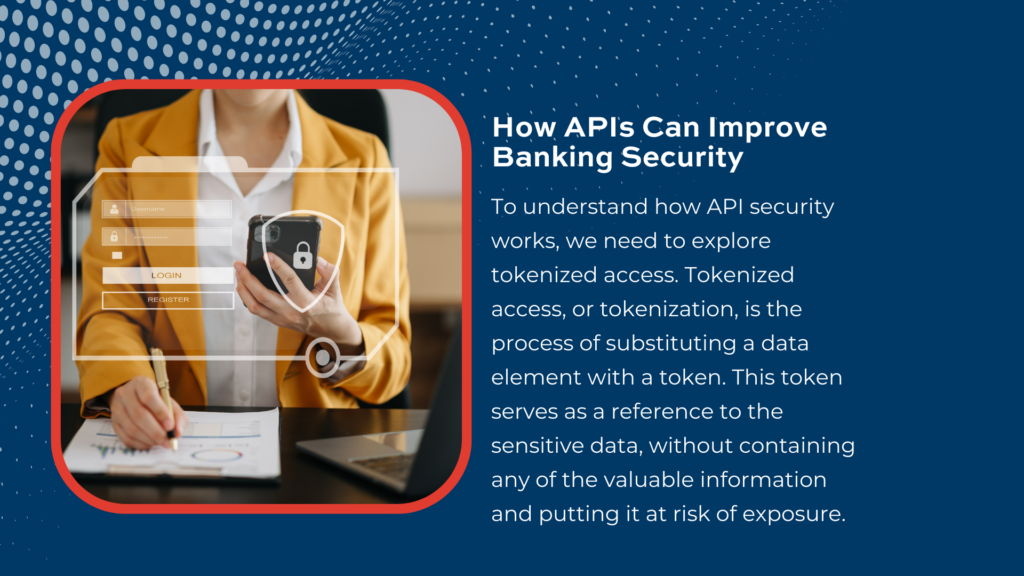

You may be wondering how APIs work to improve banking security? To understand how API security works, we need to explore tokenized access. Tokenized access, or tokenization, is the process of substituting a data element with a token. This token serves as a reference to the sensitive data, without containing any of the valuable information and putting it at risk of exposure.

This tokenization prevents reverse engineering. If a security incident does occur, the token will be exposed, as opposed to private, sensitive data.

An example of tokenized access is OAuth or Open Authorization connections. OAuth 2.0 is the current standard for API security and tokenized access. It is easy to implement, allows for token to be revoked if needed (i.e. in the case of suspicious activity), and it is compatible with other APIs.

Another API security protocol is OpenID Connect or OIDC. OpenID Connect works with OAuth 2.0. It allows individuals to use single sign-on or SSO to access sites. That means a user only has to sign in once but receives access to multiple sites or applications. OIDC allows third-party applications to verify an end user’s identity and retrieve essential profile details. The key difference between OIDC and OAuth, is simply that OIDC authenticates a user, while OAuth limits what each user is allowed to do.

When combined, the two banking APIs work together, allowing for a user to both safely sign in and retrieve data.

APIs not only make banking convenient, but also help mitigate risk. IT departments, tech teams and developers monitor a few API basics to ensure ongoing API security:

- Know how many APIs exist in their environment, and keep track of them

- Catalog APIs, recording what information they handle and how

- Conduct regular API security audits, determining existing and potential risks

Find More Security Solutions

API security plays a huge role in keeping the customers of financial institutions safe, preventing unauthorized access to sensitive data. Moreover, banking APIs have proven to have a major impact on customer satisfaction, offering greater convenience and security.

Coupled with a comprehensive branch transformation plan, today’s branch managers can offer employees and customers world class banking services that are safe, secure and seamless.

For more information on how Wittenbach keeps our clients’ locations safe, contact us, or schedule a tour of the WIttenbach Solutions Center, where you can explore options for keeping your branch locations safe, while keeping customers safe and satisfied.