The branch experience continues to evolve, and financial institutions are leaning into new ways to accommodate the accessibility needs of clients who may otherwise experience difficulty, unease, or roadblocks when transacting in person. Banks and credit unions uniquely offer high-touch customer service interactions, especially in the context of significant deposits and withdrawals or life changes such as marriage, divorce, or starting a new business. While the branch transformation process involves optimizing space and security, driving employee efficiency and empowerment, and modernizing technology, the end goal is threefold: to delight customers, to meet them where they are, and in the simplest terms, to include them.

When we consider setting up a new strategic partnership, we look across industry-leading manufacturers to pinpoint products whose technology keeps pace with accessibility goals and requirements. It’s from this perspective that we put forth three considerations for your financial institution to explore when beginning to plan your branch transformation to accommodate and delight clients with disabilities. The first offers guidance on principles to consider when approaching branch accessibility. The second area illustrates how to put these principles into action. And finally, we conclude with an emphasis on ensuring proper employee training and budget for the above will make the most of these accessibility features and investments.

Accessibility policies for financial institutions

The Americans with Disabilities Act, or ADA, operates under five titles, regulated and enforced by the U.S. Department of Justice. These laws, which cover the categories of Employment, Public Services, Public Accommodations, Telecommunications, and a Miscellaneous catch-all, extend to the banking industry in many ways. In brick-and-mortar branches of banks and credit unions, the ADA Title III is the biggest influence, requiring “reasonable modifications” for clients with physical, vision, hearing, and speech disabilities. Not only must clients legally be treated with equality, it is good business practice and humanity to do so.

The ADA Southwest says, “Banks [and credit unions] also have obligations under the Community Reinvestment Act to meet the credit needs of low- and moderate-income individuals, many of whom are people with disabilities. Thirty-two years after the enactment of the ADA, the Federal Deposit Insurance Corporation (FDIC) finds that people with disabilities are three times more likely to be unbanked compared to adults without disabilities. Additionally, even if people with disabilities are banked, they are less likely to use the full array of bank services.”

While leaning toward in-person banking, disabled individuals may also visit your website to learn about accessibility features at your branch, or to find a nearby location. Brailleworks says, “Website accessibility is especially important because it’s the easiest to catch and, therefore, the easiest to fine. […] Next, all standard forms and documents that deal with terms and conditions of doing business with your company need to be available in an accessible format like braille. Also, you need to offer all of your clients their individual banking forms and statements in an accessible format they can read. Remember, a person’s independence and freedom to read information on their own is a civil right.”

In order to accommodate and delight clients, as well as avoid costly penalties for not following ADA rules, many financial institutions have implemented an accessibility plan. A global banking association has assembled a guide entitled “Every Customer Counts”, in which they discuss design principles to bear in mind when accommodating those with disabilities, and much more. An accessibility plan will also serve to inform your branch transformation projects. When updating client-facing branch spaces and technology such as Interactive Teller Machines (ITMs), your branch’s product and design choices should factor in the legal requirements from the ADA and a customer service mindset that is functional and inviting to all clients. Examples of ITM accessibility features include open front access for wheelchair users, adjustable sound settings and a headphone jack for listening devices, screen color contrast settings, speech or keyboard input, and placement that makes it detectable by visually impaired clients who use assistive canes to help determine their surroundings.

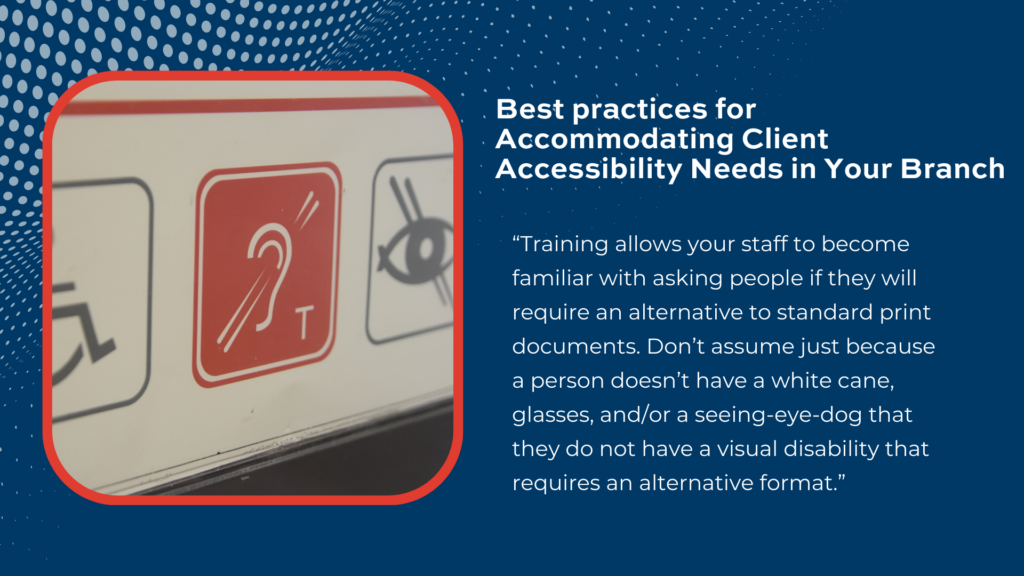

Best practices for accommodating client accessibility needs in your branch

Different kinds of disabilities may require different support, and bear in mind that accommodations are personal and on an individual basis. The number one priority is to treat every client with dignity, be patient, and do not make assumptions about an individual client’s needs or preferences without asking.

Training your staff is critical to successful interactions with disabled clients, both before, during, and after a transaction occurs. If a client is vision-impaired, your staff may offer guidance such as letting them know that they’re next in line, providing clear instructions on where the teller’s counter is, as well as explaining that the counter is raised. For physically disabled patrons, ensuring a clear path for mobility devices and uninterrupted access for service animals can provide both necessary and comfortable means of transacting.

During an in-person banking experience, having large-print and even braille forms, documents, and transaction statements can also make the experience much smoother, and meet ADA requirements. Brailleworks says, “Training allows your staff to become familiar with asking people if they will require an alternative to standard print documents. Don’t assume just because a person doesn’t have a white cane, glasses, and/or a seeing-eye-dog that they do not have a visual disability that requires an alternative format.”

For clients with hearing impairment, your employees can try to minimize background noise, speak clearly and slowly so that words can be determined, and patiently trying different ways of saying the same thing if the initial message cannot be conveyed. Directions and numbers can also be conveyed in writing for ease of use, since many sound alike.

Concluding any transaction with a disabled client should result in a recap ensuring they were able to receive all information they needed, that all transactions were completed, and that a clear, safe path is available to exit the branch.

In summary

Understanding the responsibilities of accessibility accommodation and equal treatment across all clients, regardless of disability status, is both a legal requirement and the human, ethical thing to do. Any individual might need a disability accommodation at some point in life, so being able to provide a client extra assistance who needs it will not only serve their ongoing financial stability, but will build your branch’s reputation and strengthen your mutual relationship. Contact Wittenbach’s experts today to learn more about outfitting your branches with accessibility-minded processes and products, as well as to address all of your branch transformation needs.