When exploring which option might be best for your business, either the automated teller machine (ATM) or interactive teller machine (ITM), it is important to understand the key differences between them. At Wittenbach, we keep current with the new features, services and options available in the ATM and ITM marketplace to help our customers make the best decisions about ATM and ITM purchases or branch transformation plans. In this blog, we explore the three key differentiating features between the ATM and the ITM: Automated vs. Video Services, Hardware and Software Differences and Cost and Time required for installation to help determine which machines will serve your customers best.

For years, financial institutions have implemented ATMs for use by their customers. While largely used in the beginning to withdraw cash, the added features, such as ATM with deposit, for example, made it possible to make deposits and withdrawals, without interacting with an in-person teller or even having to enter their bank or credit union. This revolutionized the banking experience for the client and the teller alike, by allowing the client to minimize the amount of time taken out of their day, without sacrificing any quality of the banking experience.

An “interactive teller machine”, or ITM, offers more features to a customer than an ATM – they are like an ATM with live, video chat. An ITM, uses a combination of touch screens and video technology to offer a virtual version of the in-person banking experience. Customers can walk up to the ITM, press begin, and start a video conversation with a live operator based anywhere in the world. This operator functions just like a bank teller inside a normal bank and can perform a variety of services for the customer. Some banks also like to keep an ITM open outside of normal banking hours to give customers more flexibility. Since an ITM offers the function of a video teller, a larger variety of bill denominations available, and extended hours of operation, among other services, which we explore more deeply below.

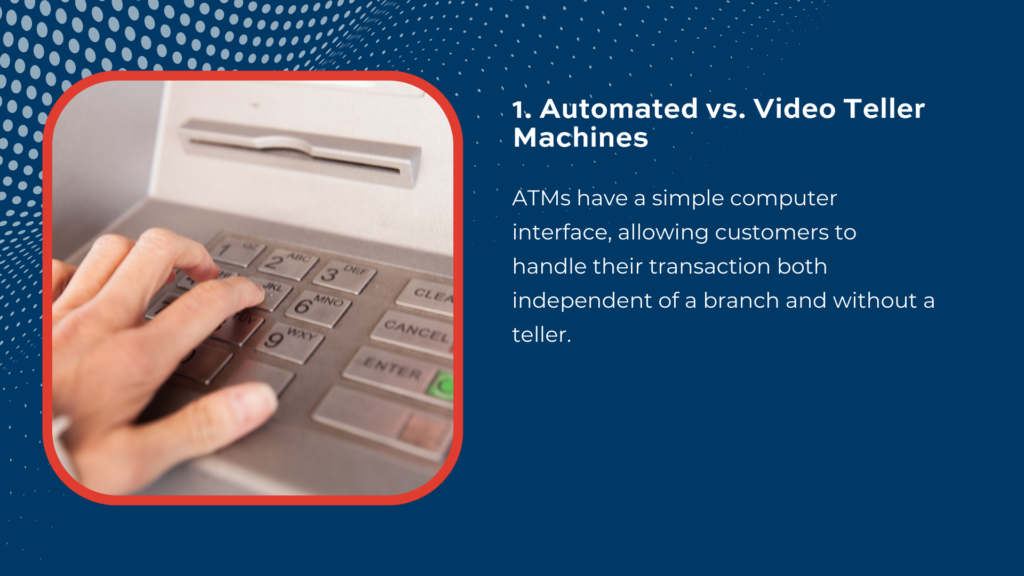

1. Automated vs. Video Teller Machines

First, the fundamental purpose of ATMs is to dispense cash, accept cash deposits, and occasionally process simple banking transactions, such as balance transfers. ATMs typically consist of a screen, a card reader, a keypad, a cash dispenser and a printer. They are often found independently operated in restaurants and various entertainment venues, in addition to being institution-branded by either a bank or a credit union. ATMs have a simple computer interface, allowing customers to handle their transaction both independent of a branch and without a teller.

ITMs, similarly, can offer an innovative alternate method of personal contact with a teller. However, the video teller function within ITMs is much more advanced in regards to offering a personal and interactive user experience to the customer. The video teller is a live person on the other side of the screen, which uses electronic signatures and ID verification to perform pretty much any service needed and allows for expanded service hours and an opportunity to answer real questions.

2. Hardware and Software Differences

Retail ATM software generally runs on Windows 10. Financial ATMs run on Money Plus software. Some ATM manufacturers tend to charge for a software suite, depending on the abilities of the machine. For simple cash dispensing, a normal ATM software package can cost around $2,000, according to Tellerex. For machines with more complex software functions, including deposit automation, a software package can cost up to $3,000. Of course, there are also optional software upgrades and subscriptions which involve additional costs.

ITM software overall is a much larger investment as compared to ATMs. ITMs operate with sophisticated software that is much more expensive and requires updates as the technology advances over time. Because the ITMs allow for a virtual experience, as opposed to one which is fully automated, the experience for the client is much richer. Because ITMs connect clients with real tellers, the machines often require updates. These ongoing fees can add up over time, making this the more expensive option.

While used ATMs might cost less than a brand new machine, which can cost upwards of $50,0000, newer ATMs have better features, such as cash recycling. Cash recycling is important because the ATM’s funds are able to be replenished less frequently, which both saves time for employees and maximizes profitability. Further, older ATMs may appear outdated and therefore dissuade customers from using them, lest the clients think they could receive better and more secure services elsewhere.

3. Cost and Time

Overall, ITMs are more expensive than ATMs. The initial order for an inaugural ITM fleet can fall between $250,000 and $750,000, which of course covers multiple machines. While a higher cost, this investment is offset through the savings realized by less staffing needed once the ITMs are fully operational. According to the American Bankers Association, financial institutions which use ITMs have a ratio of one call center ITM service agent for every 2.4 machines. Of course, fully implementing an ITM likewise involves training and staff planning to make sure it gets introduced and used fully, which likewise takes more time and discernment. Depending on your institution’s needs near and longer term, staffing resources, and plans, the higher level of service and capability that ITMs may make it the right choice for your organization.

When deciding between the ATM and the ITM, it is also important to keep in mind your institution’s time frame. Regardless of which machine you choose, it takes time to both pay for and install it.

However, if you’re on an especially tight timeline to install a new machine, and you only require a few customary features, such as cash withdrawal and cash deposits, as mentioned above, it may make more sense to order an ATM. Industry average installation time for ATMs can be around two to four weeks. If you have the time and resources to adopt new features over time, then the ITM could be of greater value to your organization. An ATM, however, is not only convenient and easy to use, but is also something a lot of customers are already familiar with and feel comfortable using, and can be operational within these few short weeks.

Adding an ITM sets the stage for the next possible advances and features of financial self-service. ITMs are valuable because they are the newest technological advancements in the banking industry, and can really improve the uptime of a business. The type of business which must align with this investment is one which looks toward the future, and which is not hesitant to follow the latest updates and breakthroughs.

In Summary

There are a few reasons why a business’ needs might be met better by an ATM over an ITM, so it is important to understand the similarities and differences that the two solutions offer. Though they seem to be quite the same at first glance, the two types of teller machines differ most prominently in regards the customer’s user experience, the hardware and software, and the cost and time required for installation.

Which machine an institution should choose fully depends on what features they require. Regarding offering the best ROI, or return on investment, there are various ATMs and ITMs Wittenbach recommends. To figure out which is best for you, Wittenbach offers consultations in which we learn about your organization, your unique needs, budget and plans for the future, so we can provide you with the details necessary for an informed decision and plan for acquisition, installation, training, and implementation.

Would you like to learn more about ATMs and ITMs? Just check out these topics, and more, on the Wittenbach blog: Exploring Wittenbach’s Foundational Pillars: ATMs and ITMs, 7 Consumer Benefits Driving ATM Market Growth, and how ATMs and ITMs can enhance accessibility.